Biotechnology, Health Plans and Pharmaceutical Retailers Faring Better Than

Others Under the Affordable Care Act; Medical Care Providers – Not So Much

Its been 5 years since President

Obama signed the Patient Protection and Affordable Care Act (PPACA or, ACA) into

law. The law promised significant changes in the landscape, with “sacrifices”

expected from each sector, in the interest of funding the expansion of coverage

to previously-uninsured Americans. In the intervening years, healthcare

organizations have been moving rapidly to redefine their business models to

survive and prosper in the post-ACA world. We now have an idea of which sectors

have gained the most, and which have struggled.

ACA included provisions that

negatively impacted several industry sectors. For instance:

- a 2.3% excise tax was placed on the medical device manufacturers, for the (non-retail) sale of their products

- insurers were required to keep administrative costs to 15% or less of premium dollars (for large group employers; 20% for small group or individual insurers). Also, no exclusions could be made for pre-existing conditions

- Medicare reimbursement to hospitals, home health agencies, hospices and skilled nursing facilities would be reduced by $716 billion over 10 years

- the Medicaid drug rebate for brand name drugs, paid by drug manufacturers to the states was increased to 23.1%.

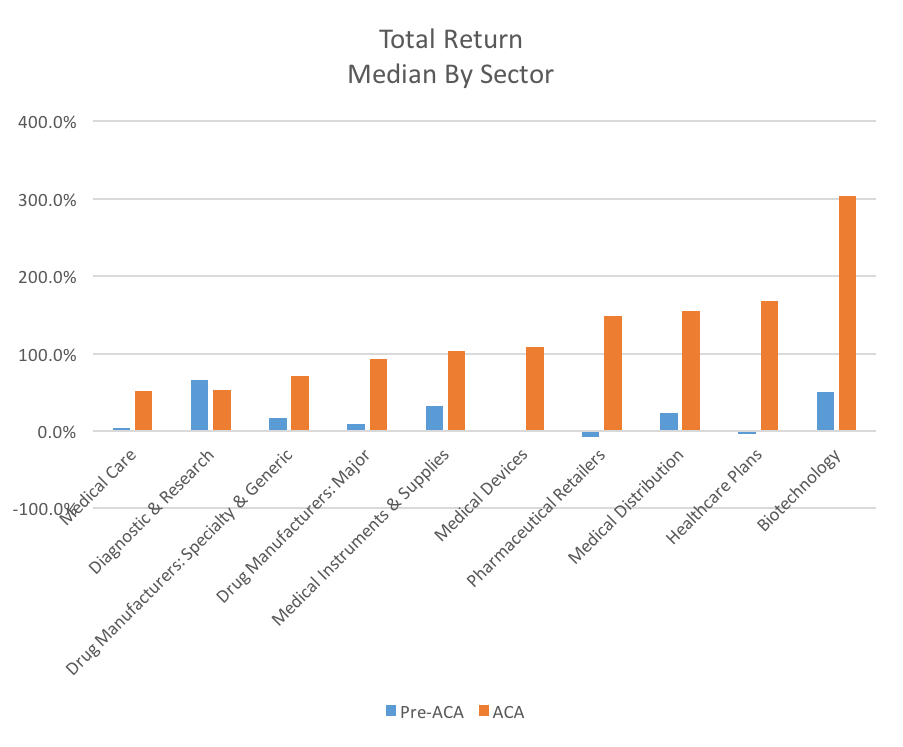

So, in the intervening 5 years,

which sectors have fared best? To answer

this question, we studied financial data from 150 public-traded health care

organizations, from across ten sectors. In particular, we reviewed each company’s Total Return[1]

during the period 2011-2015 (“ACA”), as well as a comparable 5-year period (2006-2010)

immediately preceding ACA passage (“pre-ACA”). We considered this,

sector-by-sector, from three perspectives:

- Which sectors posted the strongest median Total Return performance under ACA?

- Which sectors showed the best improvement (in median Total Return) from pre-ACA to ACA?

- Which sectors demonstrated strong performance both before and after ACA passage?

Healthcare Plans showed a

significant benefit from ACA: this

sector enjoyed the second-best performance during the period under ACA, after experiencing

the second-lowest performance during pre-ACA. Pharmaceutical Retailers similarly

showed relatively strong performance since ACA, following negative

median Total Return pre-ACA. Clearly,

these organizations are faring much better since ACA was enacted and their

business models appear well-suited to the new health care delivery system.

Surprisingly, Drug Manufacturers,

both Major and Specialty & Generic, have not experienced outsized

performance since ACA nor have they disproportionately improved from pre-ACA to

ACA. This seems to run counter to the

prevalent concerns about profiteering and rising drug costs and their impact on

overall health spending.

Notably, all sectors showed

improvement from pre-ACA to ACA. Whether this means they are better off under

ACA is debatable, however, as the earlier period included the economic

recession of 2007 and subsequent slow recovery.

So, what does all this mean going

forward? Clearly, Biotechnology companies and Pharmaceutical Retailers have

been well-positioned to promote and benefit from the shift in health care

delivery and financing. Health plans

have gained from the increased number of Americans with access to

insurance. Yet, providers (hospitals, physicians)

continue to struggle with lower reimbursement and the shift away from acute

care. Medical devices manufacturers

similarly have been impacted by lower-than expected demand, as well as the medical

device tax (since suspended).

Some of these effects could be

mitigated, however, should utilization rebound to pre-ACA (and pre-recession) levels. Some analysts, including the Centers for

Medicare & Medicaid Services, project higher utilization as more Americans

gain insurance coverage and as the US economy continues to recover from the

recession. If these projections hold true, Medical Care providers and Device manufacturers

might (finally) enjoy the increased demand that was “promised” with ACA

passage. Conversely, this would increase the cost of business for Health Plans.

(Note, for further discussion of factors which might increase utilization,

please refer to my earlier blog, Despite our best efforts, will demand drive health care expenditures to new heights?)

Mark Van Sumeren

Health Industry Advisor LLC

No comments:

Post a Comment